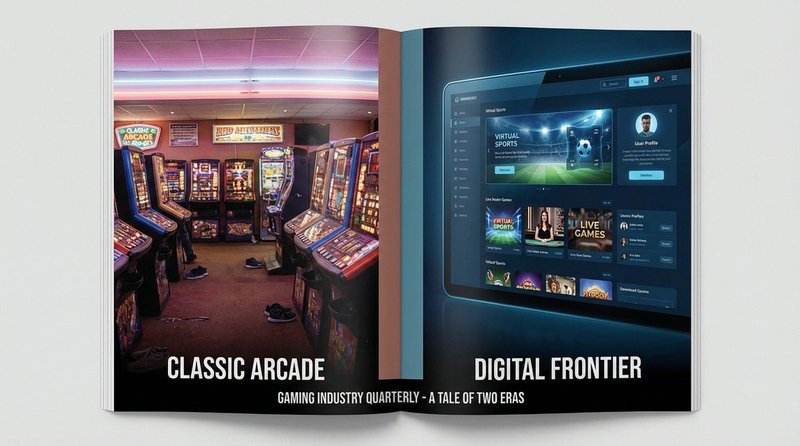

The economics of a gaming machine change fundamentally when it moves from a physical arcade floor to a digital platform. Revenue per square metre, marginal cost per play, capital expenditure profiles and customer acquisition models all diverge. For operators and suppliers working in the UK amusements sector, understanding the business model on the other side of the divide is increasingly relevant — not least because the same companies are now working both.

Revenue Models: Per-Play vs Per-Session Economics

The core metric differs completely between the two environments. Physical gaming machine revenue is the sum of coins and notes inserted minus prizes paid out. Online revenue is deposits minus withdrawals minus bonuses. That difference in accounting structures reflects a deeper difference in how value is created and captured.

For physical operators, machine performance benchmarks in the UK vary by category and venue quality. A Category C AWP in a well-run Adult Gaming Centre typically generates £200–£400 per week. Redemption cabinets in a strong FEC run £100–£300 per week. Video upright cabinets £80–£200 per week. These figures are location-dependent in a direct, unavoidable sense: if footfall falls, revenue falls. There is no marketing campaign that replaces a bad site.

Online operators measure revenue per active user per month (ARPU) as the primary commercial metric. That figure is marketing-dependent rather than location-dependent. Customer acquisition cost (CAC) — what it costs to bring in one depositing player — determines whether the unit economics work. A depositing player with a lifetime value below their acquisition cost is a net loss however active they appear in the short term.

The physical operator’s core operating metric is revenue per square metre. A compact redemption cabinet generating £250 per week from a 0.6m² footprint often outperforms a large sit-down simulator generating £400 per week from 2.5m². Online operators have no equivalent spatial constraint. Adding one thousand more players costs server capacity, not floor space. That asymmetry in marginal economics — close to zero online, significant and permanent for physical — is the fundamental structural difference between the two models.

Capital Expenditure and Operating Costs

The two models carry entirely different capex and opex profiles, which drives different financing requirements and different risk structures for operators entering either sector.

Physical arcade capex starts with cabinet purchase: new units range from £2,000 for a basic Category D redemption machine to £15,000 or more for a premium motion-platform or large-format simulator. Add premises rent, business rates, utilities, staff wages, insurance and maintenance. Maintenance alone typically runs 8–15% of purchase price annually for high-throughput cabinets. Useful life is three to seven years for most cabinet types, after which the machine either requires significant refurbishment or replacement. Capital is tied up in depreciating physical assets, and the cost base is largely fixed regardless of whether the floor is busy.

Digital platform capex is front-loaded in a different way. Platform development for a credible online casino or gaming product runs £500,000 to £2 million or more before a single player deposits. That figure covers software development, UKGC remote operating licence application, payment processing integration, KYC and AML infrastructure, and regulatory compliance systems. Once live, the marginal cost per additional player is low — server and bandwidth costs scale, but not dramatically. The variable cost that scales sharply is marketing: performance marketing spend, affiliate fees, bonus offers and CRM campaigns. These are not fixed costs; they flex directly with the ambition to grow player numbers.

Content depreciation cycles also differ. A physical cabinet depreciates over years. Online game content — individual slot titles — has a commercial shelf life of three to twelve months before player interest migrates to newer releases. Game studios and platform operators run continuous development pipelines to maintain a fresh catalogue. That is not a capital cost in the traditional sense, but it is a persistent cash commitment with no physical-world equivalent.

Market Size: UK Land-Based vs Online

The scale difference between the two markets is significant and widely misunderstood within the amusements trade. The UK amusements and theme parks sector was valued at approximately £1.4 billion in 2026 (IBISWorld), with the Family Entertainment Centre segment growing at roughly 9.3% CAGR. That is a healthy growth trajectory by any measure.

The UK online gambling market, measured by gross gambling yield, reached approximately £6.4 billion in 2024–25 according to Gambling Commission data. Online is four to five times larger by revenue. The global arcade gaming market is projected at USD 16.36 billion by 2029, reflecting strong international demand — but the UK domestic land-based market operates within a specific regulatory and economic context that differs substantially from, for example, US or Asian arcade markets.

The more important observation for UK operators is that these markets are not zero-sum. FEC growth and online growth have co-existed throughout the period since the Gambling Act 2005 came into force. Land-based amusements offers something online cannot directly replicate: a physical social environment, dwell time, catering revenue, and an experience that works for groups including children. The two markets serve overlapping but not identical customer needs. Operators treating online as an existential threat to physical tend to misread the competitive dynamic.

Where land-based faces a genuine structural challenge is in adult gaming centres dependent on Category C AWP revenue. That segment — 171 licensed FECs as of 2024 compared to 220 in 2018 according to the Government’s November 2025 consultation — has declined as compliance costs rise and player behaviour shifts. Full detail on the regulatory framework governing these venues is in our guide to UK gaming machine categories and regulations.

Customer Acquisition and Retention

Physical operators acquire customers through location. The site decision is the marketing decision. A seafront arcade, a shopping centre unit, or a high street AGC each draw from a defined catchment area. Beyond signage and local presence, marketing spend is modest. The constraint is that you cannot expand the catchment without opening a new site.

Online operators acquire customers through performance marketing: pay-per-click campaigns, affiliate networks, email, social media, and sign-up bonus structures. UK online casino CAC currently runs £100–£400 or more per depositing player, depending on acquisition channel and the competitiveness of the market segment. That is a substantial number. It means an online operator must retain a player long enough to generate lifetime value that exceeds the acquisition cost before the relationship is profitable. The bonus-driven acquisition model that dominated the early UK online market has been substantially constrained by UKGC requirements around affordability and player protection, which puts upward pressure on sustainable CAC even as it reduces harm.

Retention mechanics also differ structurally. Physical venues retain customers through familiarity, social habit, the quality of the environment, and the convenience of location. Regulars return to the same seaside arcade for years. Churn is low once a customer is established. Online churn is high: players switch platforms for better bonus offers, newer game content, or simply because the registration process for a competitor takes three minutes. Loyalty programmes, CRM campaigns and personalised offers are the primary retention tools — all require ongoing technology and marketing investment.

Regulation and Compliance Costs

Both sectors operate under UKGC oversight, but the compliance cost structures differ in composition, not just scale.

A land-based AGC or licensed FEC requires a UKGC operating licence, a local authority premises licence, Challenge 25 age verification protocols, staff training records, safer gambling signage, and compliance with the Licence Conditions and Codes of Practice. Machine Games Duty applies to all Category C and most Category D cash-prize machines, adding a tax layer that online operators do not carry in the same direct form. Annual UKGC fees and premises licence renewals are the primary ongoing compliance costs. BACTA membership is standard practice for serious operators and provides sector-specific guidance and advocacy.

Online operators carry the same UKGC annual fees — at higher rates, reflecting remote licensing structures — plus a technology-intensive compliance stack: electronic KYC verification, GamStop self-exclusion integration, automated affordability checks, AML transaction monitoring, and responsible gambling intervention systems. The 2025 UKGC compliance updates tightened affordability requirements substantially, creating a permanent overhead in compliance technology that smaller operators struggle to absorb. Compliance cost as a percentage of revenue is broadly higher for online operators, but the revenue base is also significantly larger, meaning absolute compliance investment is greater.

Both sectors face the same enforcement risk. UKGC fines for compliance failures have reached £19 million (William Hill, 2023) and £6.1 million (Ladbrokes Coral, 2023) at the online end. Land-based enforcement actions are smaller in absolute terms but can include licence suspension, which is commercially terminal for a single-venue operator. Full detail on land-based compliance requirements is in our guides to UK amusement machine regulations and Gambling Commission AWP rules.

Convergence: The Operators Working Both Sides

The clearest evidence that these are not separate industries is the supplier overlap. Barcrest (now part of Light & Wonder), IGT, Novomatic and Merkur all manufacture physical cabinets for the UK land-based market and develop online slot content licensed by the UKGC. The game mechanics that play on an AGC Category C reel cabinet and the slot title on a UK-regulated online casino are often produced by the same development team, from the same base mathematics, with surface-level adaptation for the different regulatory environments.

Technology convergence is pulling physical operations in the same direction. Cashless play systems, server-based gaming, and networked cabinet management platforms are moving arcades toward the digital infrastructure that online operators already run natively. A networked AGC floor with cashless TITO, remote machine management and real-time yield reporting looks operationally more like an online platform than it does like the coin-in-coin-out arcade of twenty years ago.

The industry’s own event calendar reflects this. The co-location of EAG and ICB (formerly the International Casino and Betting conference elements now visible at major UK trade events) demonstrates that buyers, suppliers and operators increasingly need to understand both sectors. EAG 2027 will again bring land-based and digital suppliers under the same roof. At ICE Barcelona, physical cabinet manufacturers and online platform developers exhibit side by side — a visible expression of the supply chain convergence that has been building for a decade.

For a UK AGC operator considering whether to apply for a remote operating licence: the regulatory architecture is familiar, because it is the same UKGC framework. But the technology investment, the marketing model, and the talent required to operate an online casino are materially different from those required to run a physical floor. The licence is not the hard part. Building a profitable online operation from standing start, in a market where established operators have multi-year customer data and performance marketing infrastructure, is where the challenge sits. A realistic assessment of physical arcade floor economics and a parallel review of online market structure should both precede any strategic decision to cross sectors.

Frequently Asked Questions

Is land-based gaming declining in the UK?

Not across the board. The FEC segment is growing at approximately 9.3% CAGR, driven by experience-led leisure investment. Traditional AGCs — dependent on Category C AWP revenue in high-street locations — face genuine headwinds from rising costs and a shrinking estate: licensed FEC numbers fell from 220 in 2018 to 171 by 2024. But overall land-based amusements is a growing market when FECs, holiday parks and leisure venues are included in the count.

How much does it cost to start an online casino versus a UK arcade?

Very different profiles. A small to mid-size arcade fit-out typically requires £50,000–£200,000 in cabinet procurement, plus premises costs ranging from modest (short leasehold on a secondary high street) to substantial (flagship seafront unit). An online casino credibly requires £500,000–£2 million or more in technology, licensing and initial marketing outlay before generating sustainable revenue. The online model has lower ongoing fixed costs per player but requires significant upfront capital and a player acquisition strategy that works in an intensely competitive market.

Do the same companies make machines for both physical arcades and online casinos?

Many do. Barcrest (Light & Wonder), IGT, Novomatic and Merkur all develop content for physical cabinets and online platforms. The mechanics are often identical at the mathematics layer, adapted at the interface layer for the different environments. This shared supply chain is one of the clearest structural indicators that the two markets are converging rather than diverging.

The business models underpinning physical arcades and online casino platforms differ in almost every dimension — but the direction of travel is convergence, not divergence. The same companies build products for both, the same regulator oversees both, and the same underlying technology increasingly connects them. For operators and suppliers in the UK amusements trade, the online gaming market is not a separate industry — it is the other side of the same coin. Understanding how online operators approach player acquisition, retention and regulatory compliance informs better decision-making on the physical side, where the same economics are arriving in a different form through cashless, networked and data-driven machine operations.